This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License

About this document¶

This document was created using Weave.jl. The code is available in on github. The same document generates both static webpages and associated jupyter notebook.

Introduction¶

This document is a companion to my “Machine learning in economics”. Those notes discuss the recent use of machine learning in economics, with a focus on lasso and random forests. The code in those notes is written in R. This document will look at similar code in Julia.

RCall¶

If you want to use the methods of Chernozhukov and coauthors implements

in the R packaga Chernozhukov, Victor, Chris Hansen, and Martin Spindler, “[hdm]{.nocase}: High-dimensional metrics,” R Journal, 8 (2016), 185–199. or the methods of Athey and coauthors implemented

in the R package Tibshirani, Julie, Susan Athey, Stefan Wager, Rina Friedberg, Luke Miner, and Marvin Wright, “Grf: Generalized random forests (beta),” (2018). , then it makes sense to use the R pacakge. You

could simply write all your code in R. However, if you prefer using

Julia, you can just call the necessary R functions with

RCall.jl.

Here, we load the pipeline data used in the machine learning methods notes, and do some cleaning in Julia.

using RCall, DataFrames, Missings, Statistics

R"load(paste($(docdir),\"/rmd/pipelines.Rdata\",sep=\"\"))"

println(R"ls()")

data = @rget data # data on left is new Julia variable, data on right is the one in R

println(R"summary(data[,1:5])")

println(describe(data[:,1:5]))

for c in 59:107 # columns of state mileage, want missing->0

replace!(x->(ismissing(x) || isnan(x)) ? 0.0 : x, data[!,c])

end

println(describe(data[:,59:65]))

RObject{StrSxp}

[1] "#JL" "data"

RObject{StrSxp}

respondent_id report_yr report_prd major

Min. : 1.0 Min. :1991 Min. :12 Mode :logical

1st Qu.: 64.0 1st Qu.:1997 1st Qu.:12 FALSE:1192

Median :148.0 Median :2003 Median :12 TRUE :2797

Mean :184.3 Mean :2003 Mean :12 NA's :2180

3rd Qu.:214.0 3rd Qu.:2010 3rd Qu.:12

Max. :745.0 Max. :2016 Max. :12

NA's :3371

respondent_name

Centra Pipelines Minnesota Inc. : 22

Tuscarora Gas Transmission Company : 22

Eastern Shore Natural Gas Company : 22

Kern River Gas Transmission Company : 21

National Fuel Gas Supply Corporation: 21

(Other) :2938

NA's :3123

5×7 DataFrame

Row │ variable mean min median max nmissing eltype

│ Symbol Union… Any Union… Any Int64 Type

─────┼──────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────

1 │ respondent_id 184.3 1 148.0 745 0 Int64

2 │ report_yr 2003.49 1991 2003.0 2016 0 Int64

3 │ report_prd 12.0 12 12.0 12 3371 Union{Missing, Int64}

4 │ major 0.701178 false 1.0 true 2180 Union{Missing, Bool}

5 │ respondent_name Algonquin Gas Transmission Compa… Southern Natural Gas Company … 3123 Union{Missing, CategoricalValue{…

7×7 DataFrame

Row │ variable mean min median max nmissing eltype

│ Symbol Float64 Float64 Float64 Float64 Int64 Union

─────┼───────────────────────────────────────────────────────────────────────────────────────────

1 │ North Carolina 0.00358525 0.0 0.0 1.0 0 Union{Missing, Float64}

2 │ Tennessee 0.0061488 0.0 0.0 0.635202 0 Union{Missing, Float64}

3 │ Virginia 0.00552028 0.0 0.0 1.0 0 Union{Missing, Float64}

4 │ Illinois 0.0134891 0.0 0.0 1.0 0 Union{Missing, Float64}

5 │ Indiana 0.0058707 0.0 0.0 0.550302 0 Union{Missing, Float64}

6 │ Kentucky 0.0133474 0.0 0.0 1.0 0 Union{Missing, Float64}

7 │ Gulf of Mexico 0.0140981 0.0 0.0 0.825409 0 Union{Missing, Float64}

Suppose we want to estimate the coefficient on transPlant (capital) in

a partially linear model with transProfit (profit) as the outcome.

This can be done with the R function hdm::rlassoEffects.

R"library(hdm)"

completedata = dropmissing(data,[1:10..., 59:122...], disallowmissing=true)

y = completedata[!,:transProfit]

inc = .!isnan.(y)

y = y[inc]

X = completedata[inc,[6:7..., 59:121...]]

cols = [std(X[!,c])>0 for c in 1:ncol(X)]

X = X[:,cols]

est = R"rlassoEffects($(X), $(y), index=c(1:2))"

R"summary($est)"

RObject{VecSxp}

[1] "Estimates and significance testing of the effect of target variables"

Estimate. Std. Error t value Pr(>|t|)

transPlant_bal_end_yr 0.034434 0.008878 3.879 0.000105 ***

transPlant_bal_beg_yr 0.086580 0.009383 9.228 < 2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

MLJ.jl¶

MLJ.jl is a machine

learning framework for Julia. It gives a unified interface for many

machine learning algorithms and tasks. Similar R packages include

caret and MLR. scikit-learn is

a similar Python package.

For more information on MLJ see

You can see a list of models registered to work with MLJ.jl on

github,

or by calling MLJ::models().

using MLJ

models()

239-element Vector{NamedTuple{(:name, :package_name, :is_supervised, :abstr

act_type, :constructor, :deep_properties, :docstring, :fit_data_scitype, :h

uman_name, :hyperparameter_ranges, :hyperparameter_types, :hyperparameters,

:implemented_methods, :inverse_transform_scitype, :is_pure_julia, :is_wrap

per, :iteration_parameter, :load_path, :package_license, :package_url, :pac

kage_uuid, :predict_scitype, :prediction_type, :reporting_operations, :repo

rts_feature_importances, :supports_class_weights, :supports_online, :suppor

ts_training_losses, :supports_weights, :tags, :target_in_fit, :transform_sc

itype, :input_scitype, :target_scitype, :output_scitype)}}:

(name = ABODDetector, package_name = OutlierDetectionNeighbors, ... )

(name = ABODDetector, package_name = OutlierDetectionPython, ... )

(name = ARDRegressor, package_name = MLJScikitLearnInterface, ... )

(name = AdaBoostClassifier, package_name = MLJScikitLearnInterface, ... )

(name = AdaBoostRegressor, package_name = MLJScikitLearnInterface, ... )

(name = AdaBoostStumpClassifier, package_name = DecisionTree, ... )

(name = AffinityPropagation, package_name = Clustering, ... )

(name = AffinityPropagation, package_name = MLJScikitLearnInterface, ... )

(name = AgglomerativeClustering, package_name = MLJScikitLearnInterface, .

.. )

(name = AutoEncoder, package_name = BetaML, ... )

⋮

(name = TomekUndersampler, package_name = Imbalance, ... )

(name = UnivariateBoxCoxTransformer, package_name = MLJTransforms, ... )

(name = UnivariateDiscretizer, package_name = MLJTransforms, ... )

(name = UnivariateFillImputer, package_name = MLJTransforms, ... )

(name = UnivariateStandardizer, package_name = MLJTransforms, ... )

(name = UnivariateTimeTypeToContinuous, package_name = MLJTransforms, ...

)

(name = XGBoostClassifier, package_name = XGBoost, ... )

(name = XGBoostCount, package_name = XGBoost, ... )

(name = XGBoostRegressor, package_name = XGBoost, ... )

To use these models, you need the corresponding package to be installed

and loaded. The @load macro will load the needed package(s) for any

model.

Lasso = @load LassoRegressor pkg=MLJLinearModels

import MLJLinearModels ✔

MLJLinearModels.LassoRegressor

Let’s fit lasso to the same pipeline data as above.

lasso = machine(Lasso(lambda=1.0), X, y)

train,test = partition(eachindex(y), 0.6, shuffle=true)

fit!(lasso, rows=train)

yhat = predict(lasso, rows=test)

println(yhat[1:10])

println("MSE/var(y) = $(mean((y[test].-yhat).^2)/var(y[test]))")

[0.0, 0.0, 0.0, 0.0, 0.0, 0.0, 0.0, 0.0, 0.0, 0.0]

MSE/var(y) = 1.5024909580796766

That doesn’t look very good. All the predictions are zero. This could

happen when the regularization parameter, lambda, is too large.

However, in this case the problem is something else. The warning

messages indicate numeric problems when minimizing the lasso objective

function. This can happen when X is poorly scaled. The algorithm used

to compute the lasso estimates works best when the coefficients are all

roughly the same scale. The existing X’s have wildly different scales,

which causes problems. This situation is common, so MLJ.jl has

functions to standardize variables. It is likely that the hdm package

in R does something similar internally.

lasso_stdx = Pipeline(Standardizer(),

Lasso(lambda=1.0*std(y[train]),

solver=MLJLinearModels.ISTA(max_iter=10000))

)

m = machine(lasso_stdx, X, y)

fit!(m, rows=train, force=true)

yhat = predict(m , rows=test)

println("MSE/var(y) = $(mean((y[test].-yhat).^2)/var(y[test]))")

# Get the fitted coefficients

coef = fitted_params(m).lasso_regressor.coefs

intercept = fitted_params(m).lasso_regressor.intercept

sum(abs(c[2])>1e-8 for c in coef) # number non-zero

MSE/var(y) = 0.9994939567244565

0

If we want to tune lambda using cross-validation, we can use the

range and TunedModel functions.

r = range(lasso_stdx, :(lasso_regressor.lambda), lower=1e1, upper=1e10, scale=:log)

t=TunedModel(model=lasso_stdx,

resampling=CV(nfolds=5),

tuning=Grid(resolution=10),

ranges=r,

measure=rms)

m = machine(t, X, y)

fit!(m, rows=train, verbosity=1)

yhat = predict(m , rows=test)

println("MSE/var(y) = $(mean((y[test].-yhat).^2)/var(y[test]))")

MSE/var(y) = 0.15134783267464927

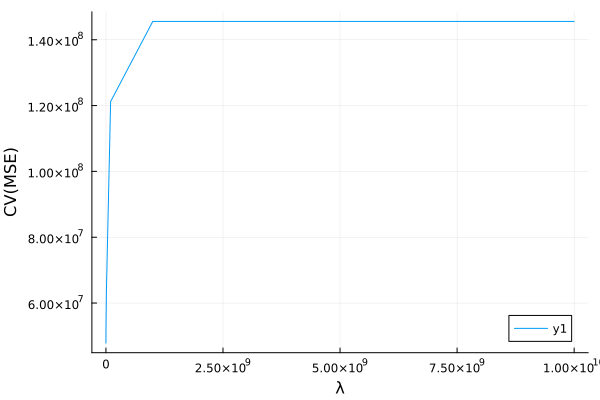

using Plots

cvmse = report(m).plotting.measurements

λ = Float64.(report(m).plotting.parameter_values[:])

s = sortperm(λ)

plot(λ[s], cvmse[s], xlab="λ", ylab="CV(MSE)")

Flux.jl¶

Flux.jl is another Julia package

for machine learning. It seems to be emerging as the leading Julia

package for neural networks and deep learning, but other machine

learning models can also be implemented using Flux.jl.

Let’s create a lasso model in Flux.jl.

using Flux, LinearAlgebra

# Scale the variables

Xstd = Flux.normalise(Matrix(X), dims=1)

X_train = Xstd[train,:]

X_test = Xstd[test,:]

yscale = std(y[train])

ymean = mean(y[train])

ystd = (y .- ymean)./yscale

y_train = ystd[train]

y_test = ystd[test]

# Set up the model parameters and initial values

βols = (X_train'*X_train) \ (X_train'*(y_train .- mean(y_train)))

β = zeros(ncol(X))

b = mean(y_train)

# Define the loss function

ψ = ones(length(β))

λ = 2.0

mutable struct LinearModel

β::Vector{Float64}

b::Float64

end

pred(m::LinearModel,x) = m.b .+ x*m.β

mse(m::LinearModel,x,y) = mean( (pred(m,x) .- y).^2 )

penalty(m::LinearModel,y) = λ/length(y)*norm(ψ.*m.β,1)

loss(m::LinearModel,x,y) = mse(m,x,y) + penalty(m,y)

m = LinearModel(β,b)

@show loss(m,X_train,y_train)

# minimize loss

maxiter=2000

obj = zeros(maxiter)

mse_train = zeros(maxiter)

mse_test = zeros(maxiter)

opt = Flux.setup(Flux.AMSGrad(), m)

import ProgressMeter: @showprogress

@showprogress for i in 1:maxiter

Flux.train!(loss, m, [(X_train, y_train)], opt)

mse_train[i] = mse(m,X_train,y_train)

mse_test[i] = mse(m,X_test, y_test)

obj[i] = loss(m,X_train,y_train)

end

lo = 1

hi = 2000

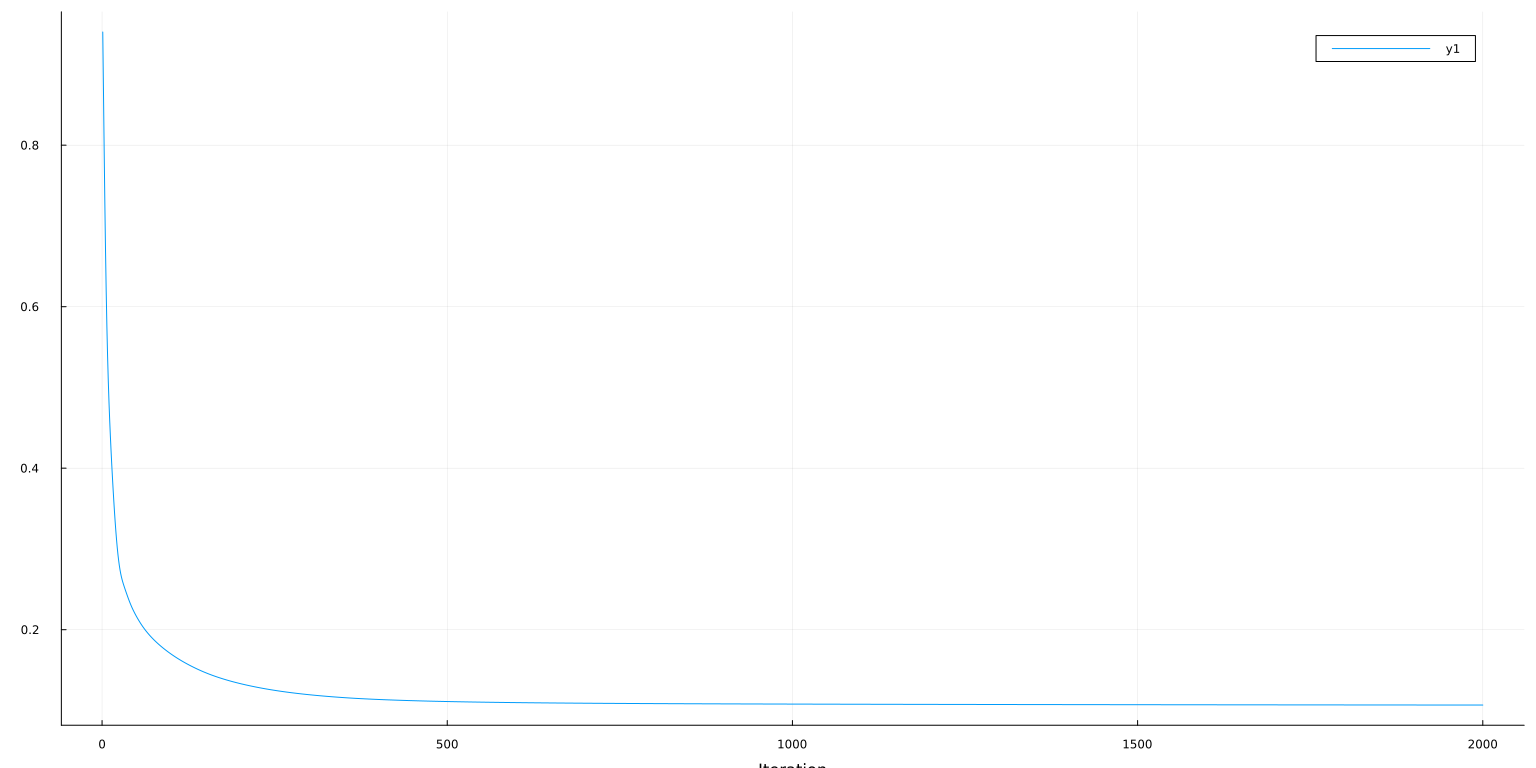

plot(obj[lo:hi], ylab="Loss=MSE + λ/n*||β||₁", xlab="Iteration")

loss(m, X_train, y_train) = 0.9986320109439124

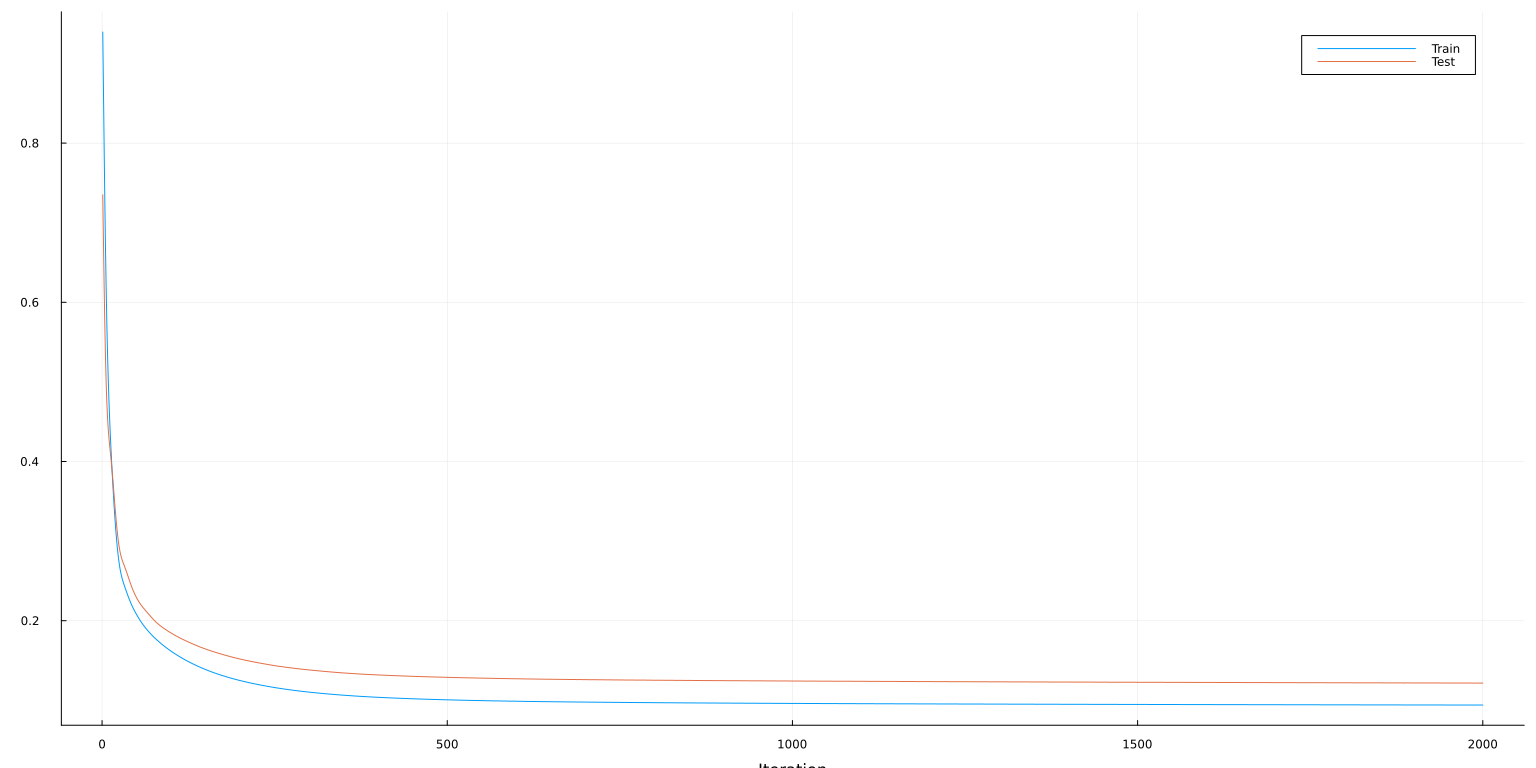

plot(lo:hi, [mse_train[lo:hi] mse_test[lo:hi]], ylab="MSE", xaxis=("Iteration"), lab=["Train" "Test"])

The minimization methods in Flux.train! are all variants of gradient

descent. Each call to Flux.train! runs one iteration of the specified

solver. To find a local minimum, Flux.train! can be called repeatedly

until progress stops. The above loop is a simple way to do this. The

@epoch macro can also be useful.

Gradient descent works well for neural networks, but is not ideal for Lasso. Without further adjustment, gradient descent gets stuck in a cycle as jumps from one side of the other of the absolute value in the lasso penalty. Nonetheless, the results are near the true minimum, even though it never exactly gets there.

Lux.jl¶

A promising alternative to Flux.jl is

Lux.jl.1 Lux.jl and Flux.jl

share many features and backend code. Lux.jl has a more function

focused interface with explicit parameter passing. This is a more

“Julian” style of programming.2

For comparison, let’s implement the same Lasso model in Lux.

import Lux # Lux shares many function names with Flux, so import instead of using to avoid confusion

import Random, Zygote

using Test

# Seeding

rng = Random.default_rng()

Random.seed!(rng, 0)

# define the model

X_train = Matrix(X)[train,:]

X_test = Matrix(X)[test,:]

y_train = y[train]

y_test = y[test]

function standardizer(xtrain)

m = std(xtrain, dims=1)

s = std(xtrain, dims=1)

(x->(x .- m)./s , xs->xs.*s .+ m)

end

stdizex, _ = standardizer(X_train)

stdizey, unstdizey = standardizer(y_train)

@test unstdizey(stdizey(y_test)) ≈ y_test

ys = stdizey(y_train)

Xs = stdizex(X_train)

# Set up the model parameters and initial values

βols = (Xs'*Xs) \ (Xs'*(ys .- mean(ys)))

b = [mean(ys)]

m = Lux.Chain(X->stdizex(X)',

Lux.Dense(size(X_train,2), 1)

)

ps, st = Lux.setup(rng, m)

ps.layer_2.weight .= βols'

ps.layer_2.bias .= b

mse(m, ps, st, X, y) = mean(abs2, m(X, ps, st)[1]' .- stdizey(y))

mseraw(m,ps,st,X,y) = mean(abs2, unstdizey(m(X, ps, st)[1]') .- y)

ℓ = let λ = 2.0, ψ = ones(size(βols')), st=st

penalty(ps,y) = λ/length(y)*norm(ψ.*ps.layer_2.weight,1)

loss(ps, X, y, m) = mse(m, ps, st, X, y) + penalty(ps,y)

end

@show ℓ(ps,X_train,y_train,m)

# minimize loss

import Optimisers

function train_model(m, initial_params, st; maxiter=2000)

opt = Optimisers.AMSGrad()

ps = initial_params

optstate = Optimisers.setup(opt, ps)

obj = zeros(maxiter)

mse_train = zeros(maxiter)

mse_test = zeros(maxiter)

@showprogress for i in 1:maxiter

# Compute the gradient

gs = Zygote.gradient(ps->ℓ(ps, X_train, y_train, m), ps)[1]

# Perform parameter update

optstate, ps = Optimisers.update(optstate, ps, gs)

mse_train[i] = mse(m, ps, st, X_train,y_train)

mse_test[i] = mse(m, ps, st, X_test, y_test)

obj[i] = ℓ(ps,X_train,y_train,m)

end

return(ps, mse_train, mse_test, obj)

end

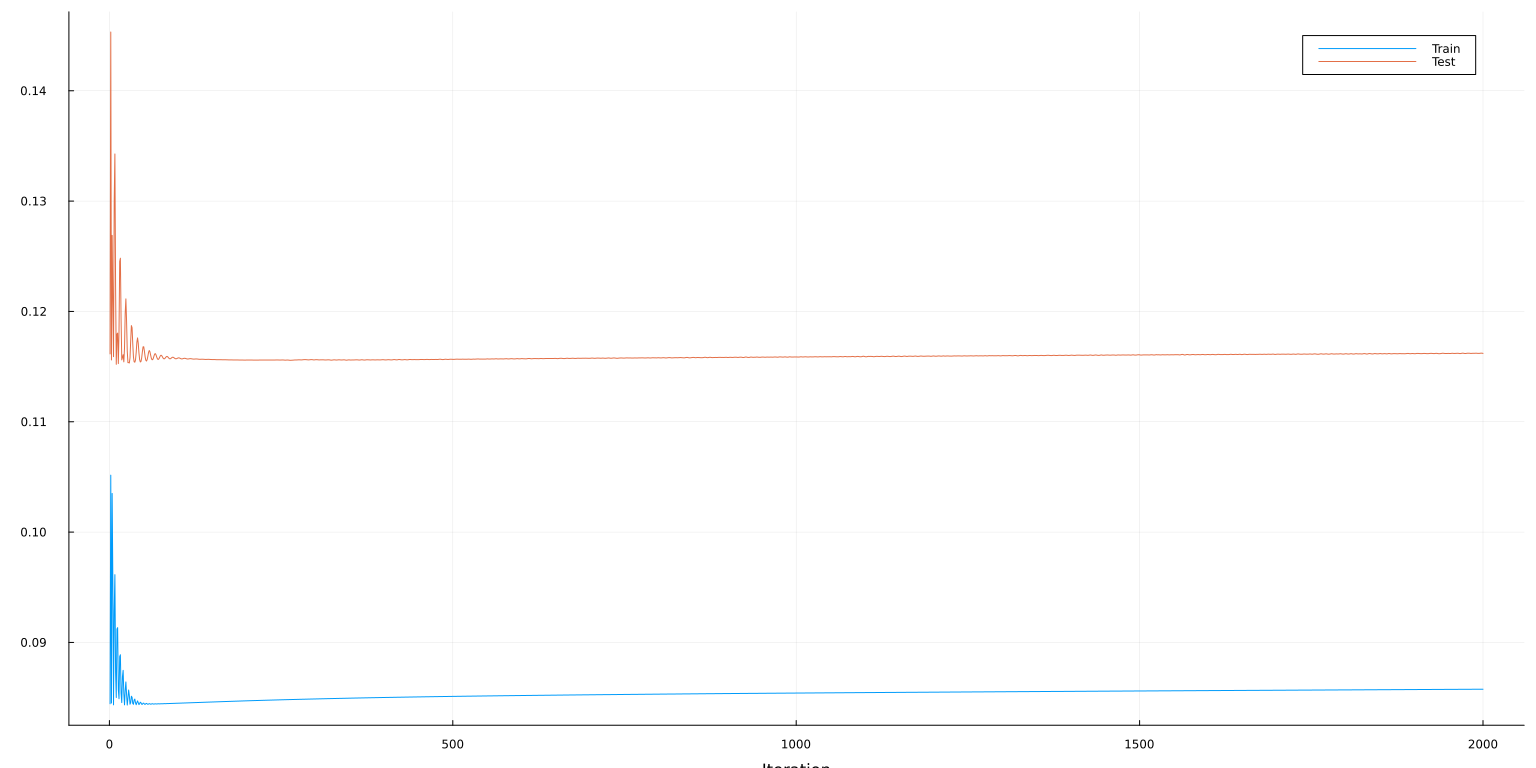

ps, mse_train, mse_test, obj = train_model(m, ps, st)

lo = 1

hi = 2000

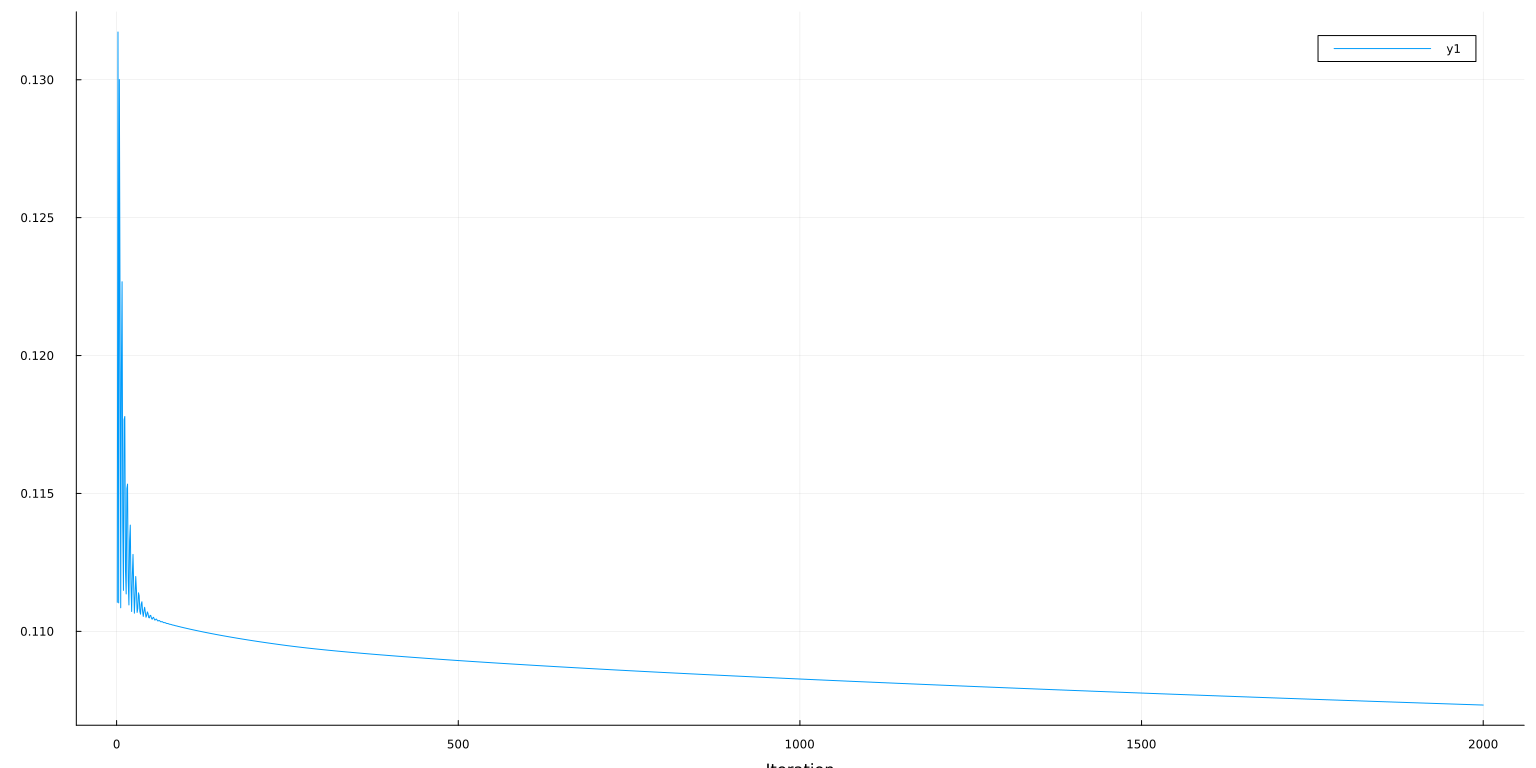

plot(lo:hi,obj[lo:hi], ylab="Loss=MSE + λ/n*||β||₁", xlab="Iteration")

ℓ(ps, X_train, y_train, m) = 0.11116189450789928

plot(lo:hi, [mse_train[lo:hi] mse_test[lo:hi]], ylab="MSE", xaxis=("Iteration"), lab=["Train" "Test"])

Additional Resources¶

- (Klok and Nazarathy 2019)3 Statistics with Julia:Fundamentals for Data Science, MachineLearning and Artificial Intelligence

References¶

-

These notes were originally written before Lux.jl existed. If I were starting over, I would use Lux.jl instead of Flux.jl. ↩

-

Flux.jldrew inspiration for its interface from Tensorflow and PyTorch. Implicit parameters makes some sense in an object oriented language like Python, but it is not the most natural style for Julia. ↩ -

Klok, Hayden, and Yoni Nazarathy, “Statistics with julia:fundamentals for data science, MachineLearning and artificial intelligence,” (DRAFT, 2019). ↩